Protect what matters most with comprehensive insurance solutions covering life, health, and assets.

Available Products

Explore our carefully curated investment options

Term Life Insurance

Health Insurance

Child Education Plan

General Insurance

Types of Insurance

Each type serves a different need—choose the right coverage for you.

Life Insurance

Life insurance is a financial product that offers the policyholder financial security in the event of an untimely death. It is essential for everyone who is employed and has dependants (spouse, children, or retired parents), since an early death would deprive the family of income and cause financial difficulty. It becomes even more important if you have debt such as a home loan or auto loan. A life insurance policy gives your dependants financial stability for a specified period (the policy term) if you die during that term. The level of protection is called the sum assured or cover—the amount your dependants receive on your untimely death during the policy term. Your cover should be enough to support your family at least until your dependants are financially independent (e.g. when your children start working) and to repay any outstanding debt. As a rule of thumb, sum assured should be at least 10–12 times your yearly income. The cost of the policy is the premium, paid annually or at other intervals (monthly, quarterly, etc.); single-payment policies are also available, with the full premium paid in advance (often with a discount). Premium depends on sum assured, your age, pre-existing conditions (e.g. diabetes, hypertension), lifestyle (e.g. smoking), and optional riders (accident, critical illness).

Sum assured: aim for at least 10–12 times your annual income; cover should support dependants until they are independent and repay debts.

Premium: paid annually or in other intervals; single-payment option with lump-sum discount. Factors: sum assured, age, health, lifestyle, riders.

Term life insurance: pure protection for the policy term; no survival benefits; if you die, dependants get sum assured; premiums are lower than other life plans.

Traditional life insurance: offers survival benefits—if you outlive the term you get the sum assured plus guaranteed additions and possibly reversionary bonuses; insurance plus investment.

ULIPs: unit linked plans combine insurance with market-linked investment (equity/debt); part of premium for cover, part invested; market risk but potential for higher returns than traditional plans.

Tax: proceeds (death or maturity) and amount invested are tax-free under Section 10(10D); no TDS on life insurance—useful for tax savings.

Life Insurance

Life insurance is a financial product that offers the policyholder financial security in the event of an untimely death. It is essential for everyone who is employed and has dependants (spouse, children, or retired parents), since an early death would deprive the family of income and cause financial difficulty. It becomes even more important if you have debt such as a home loan or auto loan. A life insurance policy gives your dependants financial stability for a specified period (the policy term) if you die during that term. The level of protection is called the sum assured or cover—the amount your dependants receive on your untimely death during the policy term. Your cover should be enough to support your family at least until your dependants are financially independent (e.g. when your children start working) and to repay any outstanding debt. As a rule of thumb, sum assured should be at least 10–12 times your yearly income. The cost of the policy is the premium, paid annually or at other intervals (monthly, quarterly, etc.); single-payment policies are also available, with the full premium paid in advance (often with a discount). Premium depends on sum assured, your age, pre-existing conditions (e.g. diabetes, hypertension), lifestyle (e.g. smoking), and optional riders (accident, critical illness).

Sum assured: aim for at least 10–12 times your annual income; cover should support dependants until they are independent and repay debts.

Premium: paid annually or in other intervals; single-payment option with lump-sum discount. Factors: sum assured, age, health, lifestyle, riders.

Term life insurance: pure protection for the policy term; no survival benefits; if you die, dependants get sum assured; premiums are lower than other life plans.

Traditional life insurance: offers survival benefits—if you outlive the term you get the sum assured plus guaranteed additions and possibly reversionary bonuses; insurance plus investment.

ULIPs: unit linked plans combine insurance with market-linked investment (equity/debt); part of premium for cover, part invested; market risk but potential for higher returns than traditional plans.

Tax: proceeds (death or maturity) and amount invested are tax-free under Section 10(10D); no TDS on life insurance—useful for tax savings.

Why Us

Features & Benefits

Why Choose our Insurance solutions

Comprehensive Coverage

Protection for life, health, and critical illness

Family Security

Secure your loved ones' financial future

Tax Savings

Claim deductions under Section 80C and 80D

Affordable Premiums

Get maximum coverage at competitive rates

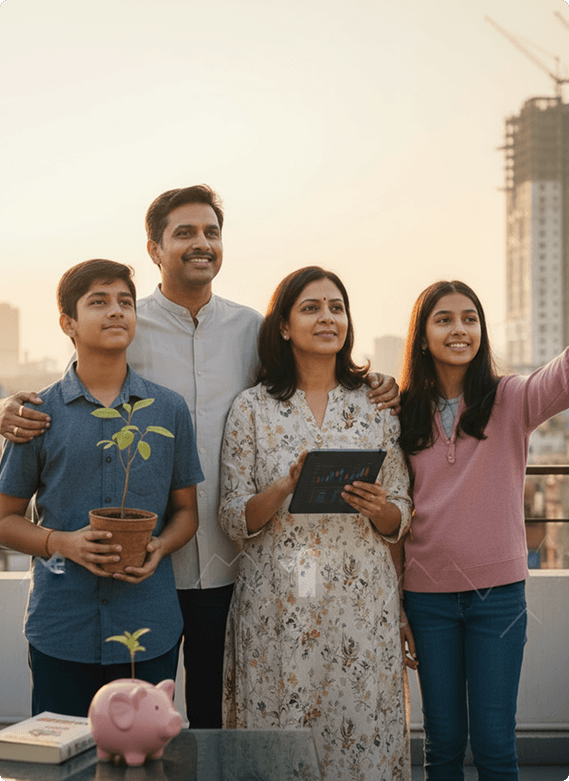

Protection for What Matters Most

Comprehensive insurance solutions for complete peace of mind

Secure your family's financial future with term plans offering coverage up to ₹5 Cr at affordable premiums starting from ₹500/month.

Enquiry

We are eager to assist you. Please provide your details and our team will get back to you shortly.